Income Statement Explained: A Complete Beginner's Guide for Small Businesses

Unpacking the Income Statement: A Beginner's Guide

Your business might be profitable on paper but still running out of cash. Here is how to read the numbers that matter.

You are not alone if the rows of numbers on your income statement leave you feeling lost. Many small business owners in the GCC face this challenge. Yet, mastering your income statement is crucial for smart decisions about pricing, expenses, and growth.

The income statement, or profit and loss (P&L) statement, tells you if your business made or lost money over a specific period. It is your financial report card, detailing not just profitability but also where your money comes from and where it goes.

Let us break down every line of the income statement, explain each number's significance, and show you how to leverage this information for a healthier business.

What is an Income Statement?

The income statement is one of the three core financial statements every business needs. It summarizes your revenues, expenses, and profits over a specific time period, typically a month, quarter, or year.

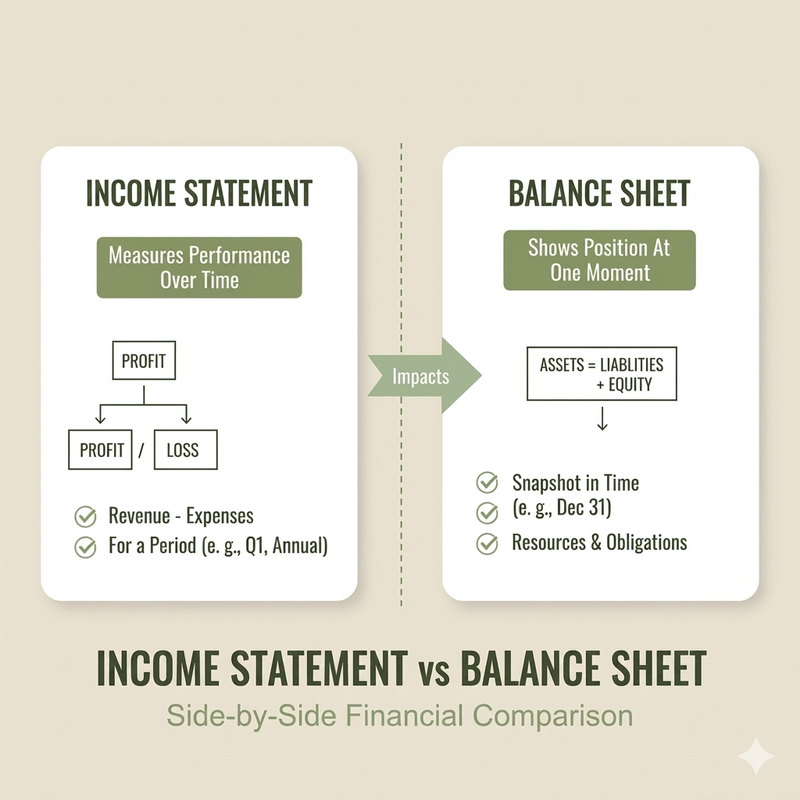

Think of it as your business scorecard. While your balance sheet shows what you own and owe at a single point in time, your income statement shows your performance over time. Did you earn more than you spent? By how much? Which products or services drove the most revenue? Which expenses are eating into your margins?

For GCC businesses navigating VAT compliance, corporate tax requirements, and e-invoicing regulations, an accurate income statement is not just useful—it is mandatory. Tax authorities in Saudi Arabia, UAE, and across the region require regular financial reporting, and your income statement forms the foundation of these reports.

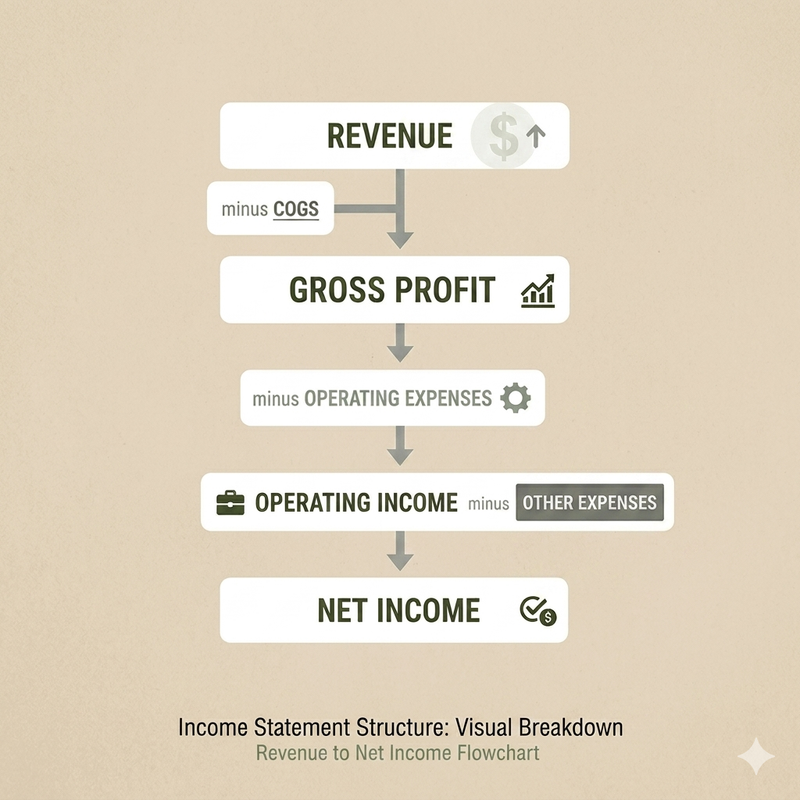

The basic structure is simple: start with revenue (what you earned), subtract expenses (what you spent), and what remains is your net income (profit or loss). But as with most things in business, the details matter. Let us unpack each component.

The Three Main Components of an Income Statement

Every income statement follows the same basic formula, regardless of whether you run a retail shop in Riyadh, a consulting firm in Dubai, or a manufacturing plant in Doha.

Revenue (Top Line)

Revenue is the total amount your business earns from selling products or services before any expenses are deducted. You will often hear it called the "top line" because it sits at the very top of your income statement.

Revenue includes all sales, whether customers have paid you yet or not. If you invoice a client in April but receive payment in May, that revenue still counts in April under accrual accounting (the standard method for most businesses).

Important distinction: gross revenue is your total sales before any deductions, while net revenue is what remains after you subtract returns, discounts, and allowances. For example, if your retail shop in Jeddah had SAR 100,000 in sales but customers returned SAR 5,000 worth of goods, your net revenue is SAR 95,000.

In the GCC, if your business is VAT-registered, revenue should typically be shown excluding VAT. The VAT you collect is not your income—it belongs to the tax authority.

Expenses (Cost of Operations)

Expenses are what you spend to generate revenue. They fall into several categories:

Cost of Goods Sold (COGS): These are direct costs tied to producing your product or delivering your service. For a bakery, COGS includes flour, sugar, and packaging. For a software company, COGS might include hosting fees and payment processing costs. COGS does not include rent, salaries, or marketing.

Operating Expenses: These are the costs of running your business day-to-day: salaries and wages, rent, utilities, marketing and advertising, insurance, and professional fees.

Other Expenses: These sit outside your normal operations, such as interest on business loans or one-time costs like equipment repairs.

Proper categorization matters. If you lump all expenses together, you cannot identify which areas are efficient and which are bleeding money.

Net Income (Bottom Line)

Net income is what remains after all expenses are subtracted from revenue. This is your profit (if positive) or loss (if negative). You will hear it called the "bottom line" because it sits at the bottom of your income statement.

Here is the key insight many business owners miss: revenue is not profit. You might have SAR 500,000 in monthly revenue, but if your expenses are SAR 520,000, you lost SAR 20,000 that month. Revenue tells you how much you sold. Net income tells you whether you made money.

For tax purposes, net income is the starting point for calculating corporate tax obligations in the UAE or zakat in Saudi Arabia. The more accurate your income statement, the fewer surprises when tax season arrives.

Reading an Income Statement: Line by Line

Let us walk through a simplified example for a small trading company in Dubai. All figures are in AED.

Revenue: The company sold AED 250,000 worth of goods this month.

COGS: It cost AED 150,000 to purchase or produce those goods.

Gross Profit: Revenue minus COGS equals AED 100,000 gross profit. This is the money available to cover operating expenses and generate profit. The gross profit margin here is 40 percent (100,000 ÷ 250,000), meaning for every dirham of sales, 40 fils goes toward covering other costs and profit.

Operating Expenses: Running the business cost AED 58,000 this month. Salaries are the largest expense, which is typical for service-oriented or small businesses.

Operating Income: Gross profit minus operating expenses equals AED 42,000. This shows how much the core business operations earned before financing costs.

Interest Expense: The company pays AED 2,000 monthly on a business loan.

Net Income: After all expenses, the company made AED 40,000 in profit. This is the "bottom line."

If you see your income statement laid out like this, you can immediately spot opportunities. For instance, if COGS suddenly jumps from 60 percent to 70 percent of revenue, you know supplier costs increased or inventory shrinkage is happening. If salaries creep from 14 percent to 25 percent of revenue without a corresponding revenue increase, you are overstaffed or underpricing.

Income Statement vs Other Financial Statements

Your income statement does not work alone. It is part of a trio of financial statements that together give you a complete picture of your business health.

Income Statement vs Balance Sheet: The income statement shows your performance over time (profit or loss), while the balance sheet shows your financial position at a single moment (what you own and owe). You can be profitable on your income statement but still have low cash if you have invested heavily in inventory or equipment, which shows up on the balance sheet.

Income Statement vs Cash Flow Statement: This is where many business owners get confused. Your income statement might show profit, but your cash flow statement shows whether you actually have cash on hand. Why? Because income statements use accrual accounting. If you invoiced AED 50,000 but customers have not paid yet, that revenue appears on your income statement even though no cash entered your bank account. The cash flow statement tracks actual money movement.

Why you need all three:

- Income statement: Are we profitable?

- Balance sheet: Do we have assets to cover our liabilities?

- Cash flow statement: Can we pay our bills this month?

Ignore any one of these, and you are flying blind.

Common Income Statement Mistakes Small Businesses Make

Even experienced business owners make these errors when interpreting income statements:

1. Confusing revenue with profit: Saying "We made AED 100,000 this month" when you mean revenue is misleading. If expenses were AED 110,000, you actually lost AED 10,000. Always clarify whether you are talking about revenue or net income.

2. Not categorizing expenses properly: Dumping all expenses into "General Expenses" makes it impossible to analyze where money goes. Break out major categories like payroll, rent, marketing, and COGS so you can identify trends.

3. Ignoring non-operating income and expenses: If you sold an old delivery van for AED 15,000, that is non-operating income. It is not part of your core business performance, so it should be listed separately from revenue. Mixing these creates a false picture of business health.

4. Reviewing too infrequently: Many small businesses only look at income statements once a year when filing taxes. By then, problems have compounded. Monthly reviews catch issues early. If your marketing spend doubled without a corresponding revenue increase, you want to know in week two, not month twelve.

5. Forgetting to account for seasonality: If you run a tourism business in Dubai, comparing your income statement from July (slow season) to December (peak season) will show wildly different results. Year-over-year comparisons (December 2025 vs December 2024) give a clearer picture.

How to Use Your Income Statement for Better Decisions

An income statement is only valuable if you act on what it tells you. Here is how smart business owners use this document:

Track profitability trends over time: Compare your income statements month-over-month and year-over-year. Is gross profit margin shrinking? Are operating expenses growing faster than revenue? These trends reveal problems before they become crises.

Identify which expenses are growing too fast: If your marketing spend increased by 50 percent but revenue only grew 10 percent, your marketing is not working efficiently. If rent now consumes 30 percent of revenue (up from 20 percent last year), you might need to renegotiate your lease or find a cheaper location.

Make informed pricing decisions: If your gross profit margin is only 20 percent but competitors operate at 40 percent, you are likely underpricing. Your income statement quantifies this. Conversely, if net income is strong but revenue growth is slow, you might have room to lower prices to capture market share.

Plan for taxes and cash flow: Your net income determines your corporate tax liability in the UAE (9 percent on profits above AED 375,000) or zakat obligations in Saudi Arabia. Reviewing your income statement quarterly lets you set aside funds for these obligations instead of scrambling when tax deadlines arrive.

Justify decisions to lenders and investors: When you need a business loan or outside investment, lenders will scrutinize your income statement. A consistent track record of profitability makes you a safer bet. Loss-making businesses can still secure funding if they show revenue growth and a clear path to profitability, but the numbers must be there.

If you are not already reviewing your income statement monthly, start today. Even fifteen minutes of review can reveal insights that save thousands of dirhams or riyals.

Make Your Income Statement Work for You

The income statement is not just a document you generate for tax authorities. It is a decision-making tool that shows whether your business model works, which expenses are justified, and where to focus your energy.

You do not need an accounting degree to read an income statement. You just need to understand the basics: revenue minus expenses equals net income. From there, the story your numbers tell becomes clear.

If reviewing financial statements still feels overwhelming, modern tools can help. Bizrah automatically generates your income statement from your daily transactions, categorizes expenses intelligently, and alerts you when margins slip—so you spend less time on manual bookkeeping and more time running your business.

Start with your most recent income statement. Read it line by line using the framework in this guide. The insights waiting in those numbers could transform how you run your business.