Accounting for Farms: Crops, Livestock, and Cash Flow

Accounting for Farms: Crops, Livestock, and Cash Flow

Your spreadsheet works fine until harvest comes and you realize you have no idea if you made money.

You planted three months ago. You spent on seeds, irrigation, labor, fertilizer. The crop looks good. You sell at harvest. But did you actually make a profit, or did the market price just barely cover your costs?

Most farm owners do not know until it is too late.

Farm accounting is not the same as accounting for a retail shop or a consulting business. Your inventory grows. Your revenue comes in bursts. Your costs accumulate for months before you see a single dirham in sales.

If you run a farm and you are still using a basic spreadsheet or relying on memory, you are flying blind. That is a problem when margins are thin and cash flow gaps can break you.

Why Farm Accounting Is Different

In most businesses, you buy inventory, you sell it, you record the profit. Clean.

Farms do not work that way.

Your inventory is alive. A calf born today is worth more next year. A date palm takes six months from pollination to harvest, and every week you spend money watering, fertilizing, and paying labor. But you cannot sell anything until the dates are ready.

This creates three specific problems that most accounting systems are not built to handle:

Biological assets — crops and livestock that grow and change value over time

Production cycles — costs accumulate over weeks or months, revenue arrives in a single transaction

Cash flow gaps — you spend now, you earn later, and the gap can be three, six, or twelve months

Most small farms in the GCC still track this on paper or in a single Excel file. That might work when you have one greenhouse or a small herd. It stops working when you scale, when you add a second crop cycle, or when you need to decide whether expanding is actually profitable.

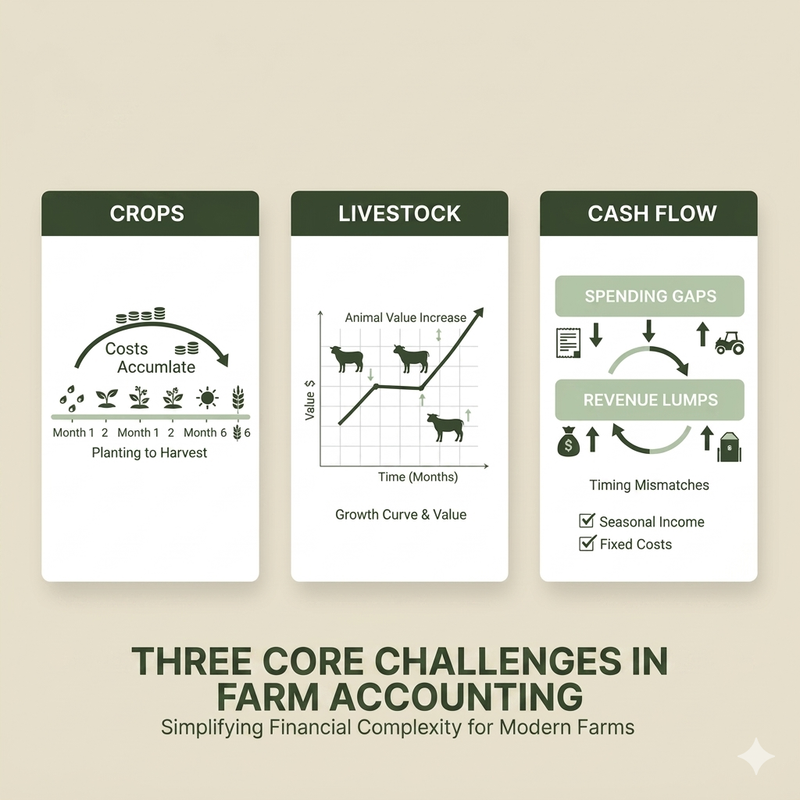

Three Core Challenges in Farm Accounting

Crops — When to Record Revenue and Costs

You plant tomatoes in January. You spend on seeds, soil prep, irrigation systems, daily labor, fertilizer, and pest control. Every week, costs go up. But you do not sell a single tomato until April.

So when do you record those costs? When do you call the crop "inventory"? When do you move it from "work in progress" to "finished goods"?

Most farmers wait until harvest and then try to remember what they spent. That is guessing, not accounting.

The correct approach is to track production costs by cycle. Every planting season or crop cycle gets its own bucket. You accumulate costs as you go: seed costs in week one, irrigation in weeks two through twelve, labor every week, fertilizer in weeks four and eight. When you harvest, you know exactly what that batch of tomatoes cost to produce.

Then you compare that total cost to the revenue from selling those tomatoes. That is how you know if you made money.

Example: A date farm in the UAE. Pollination happens in March. Dates mature over six months. Harvest is in September. During those six months, the farm spends on irrigation, labor for thinning and bagging, and pest control. If the farm does not track these costs by production cycle, it has no way to know whether this year's harvest was profitable or not.

Livestock — Growing Assets on Your Balance Sheet

A retail business buys a product for 100 dirhams and sells it for 150. Simple.

A livestock farm buys a calf for 2,000 dirhams. Then it feeds that calf for a year. The calf grows. Its market value increases. At the end of the year, the farm sells it for 5,000 dirhams.

But during that year, the calf was not just sitting there. It was eating feed, getting vet care, and consuming labor. Those are costs. At the same time, the calf itself was appreciating in value.

This creates an accounting question: do you treat the calf as inventory valued at cost (the 2,000 you paid plus accumulated feed costs)? Or do you revalue it at market price as it grows?

For small farms, the simpler approach is cost-based: track what you paid for the animal plus the costs to raise it. When you sell, you record the difference as profit.

For larger operations, especially breeding farms or dairy operations, you may need to treat mature breeding animals as fixed assets and depreciate them over their productive lifespan.

Either way, the key principle is the same: livestock is inventory that grows. If you do not track the costs that go into that growth, you cannot measure profitability accurately.

Example: A sheep farm in Saudi Arabia raises animals for Eid. The farm buys lambs at three months old, raises them for six months, and sells them during Eid season. Feed costs, vet costs, and labor all accumulate during that period. Without proper cost tracking, the farm owner might think they made a profit just because the sale price was higher than the purchase price. But if feed costs doubled that year, the profit margin might have disappeared.

Cash Flow — The Gap Between Spending and Selling

This is the challenge that breaks farms.

You spend money every week. Seeds, feed, irrigation, labor, fuel for equipment. The cash leaves your account steadily, week after week, for months.

Then you sell. One transaction. One large deposit. Then the cycle starts again.

If you do not manage this gap, you run out of cash before harvest. You cannot pay labor. You cannot buy feed. You cannot afford the next planting cycle.

This is why cash flow management is more critical for farms than for most other businesses. Revenue is lumpy. Expenses are constant. If you do not forecast your cash position, you will hit a wall.

The fix: track your cash flow by production cycle. Know when the next big expense is coming (planting, breeding season). Know when the next revenue event is (harvest, livestock sale). If the gap is too wide, you need financing to bridge it, or you need to stagger your production cycles so revenue comes in more frequently.

Many GCC farms run multiple crop cycles or multiple livestock batches specifically to smooth out cash flow. That is smart planning. But it only works if you are actually tracking cash flow.

The Accounting Basics Every Farm Needs

If you are running a farm and you want to know whether you are making money, you need a proper chart of accounts. Not the generic chart of accounts that comes with most accounting software. A chart of accounts designed for agriculture.

Here is what that looks like:

Asset Accounts

Growing crops (work in progress) — costs accumulating before harvest

Harvested crops (finished goods inventory) — ready to sell but not yet sold

Livestock inventory — animals for sale

Breeding livestock (if applicable) — animals kept for breeding, treated as fixed assets

Land — if owned

Farm equipment — tractors, irrigation systems, storage facilities

Expense Accounts

Seeds and planting materials

Feed costs (for livestock)

Fertilizer and soil amendments

Irrigation and water costs

Labor (farm workers)

Veterinary and animal health

Fuel and equipment maintenance

Packaging and storage

Revenue Accounts

Crop sales (by type: dates, tomatoes, etc.)

Livestock sales (by type: cattle, sheep, etc.)

By-product sales (milk, eggs, manure, etc.)

This structure lets you track costs by category and by production cycle. You can see which crops are profitable, which livestock batches had higher costs, and where your biggest expenses are.

Practical Steps to Get Farm Accounting Right

If you are starting from scratch or upgrading from a basic spreadsheet, here is what to do:

Track costs by production cycle — Every planting season or livestock batch gets its own identifier. Record costs against that cycle as they happen.

Use inventory categories — Separate your inventory into: inputs (seeds, feed), work in progress (growing crops, young livestock), and finished goods (harvested crops, animals ready for sale).

Separate capital expenses from operating expenses — Buying land or a new tractor is a capital expense. It goes on your balance sheet and depreciates over time. Buying seeds or feed is an operating expense. It hits your income statement immediately.

Monitor cash flow weekly during growing seasons — You do not have the luxury of monthly reviews. Cash flow gaps close fast. Check your cash position every week during high-expense periods.

Calculate cost-per-unit — What did it cost to produce one kilogram of dates? One head of livestock? This is your true profitability metric. If your cost-per-unit is higher than your selling price, you are losing money no matter how busy you feel.

Common Mistakes Farm Owners Make

Mixing Personal and Farm Expenses

You use the farm truck to run personal errands. You pay for groceries out of the farm account. You take cash from farm revenue without recording it.

This makes it impossible to know whether the farm is profitable. If you want clear financials, separate personal and business completely.

Not Tracking Inventory Properly

You guess how many animals you have. You do not count young livestock. You do not track growing crops as inventory until they are harvested.

Result: your financials are fiction. You cannot make decisions based on data you do not have.

Ignoring Depreciation

You bought a tractor five years ago for 200,000 dirhams. It is still running, so you assume it has no cost.

Wrong. That tractor is wearing out. It has a lifespan. Every year, part of its value is consumed. That is depreciation, and it is a real cost even if no cash leaves your account today.

Ignoring depreciation makes your farm look more profitable than it is. Then you are surprised when you need to replace equipment and have no money saved.

Not Planning for Seasonal Cash Flow Gaps

You assume that because you sold well at harvest, you have plenty of cash. Then six weeks later you are scrambling to pay for the next planting cycle.

Seasonal businesses need cash flow forecasting. Know when the money is coming in. Know when the big expenses hit. Plan ahead.

Treating All Spending as Expenses

You spend 500,000 dirhams on a new irrigation system. You record it as an expense. Your income statement shows a huge loss that year.

But that irrigation system will be used for ten years. It is not an expense. It is a capital investment. You depreciate it over its useful life.

Misclassifying capital expenses makes your financials misleading and makes it harder to get financing.

Why This Matters for GCC Farms

The GCC agricultural sector is growing. Governments in Saudi Arabia, UAE, and Qatar are investing in food security. Farms are expanding. But most small and mid-sized farms still run on informal accounting.

That works until it does not. When you want financing, the bank wants financials. When you want to scale, you need to know which operations are profitable. When costs spike or prices drop, you need data to make decisions fast.

If you are running a farm in the GCC and you are still using spreadsheets and memory, you are behind. The farms that will scale and survive the next ten years are the ones that treat accounting as a core operational capability, not an afterthought.

Learn more about Cash Flow vs. Profit and Accounting for Non-Accountants.

See how Bizrah handles inventory, cost tracking, and cash flow for agricultural businesses → Start free trial