Accounting for Non-Accountants: What Every Business Owner Needs to Know

Accounting for Non-Accountants: What Every Business Owner Needs to Know

You do not need a degree. You need the right mental models.

Why Most Business Owners Avoid This (And Why That Is a Problem)

Most founders treat accounting like a fire alarm.

They ignore it until something forces them to pay attention. A tax deadline. An investor due diligence request. A bank loan application. Then they scramble, hand everything to an accountant, and hope the numbers work out.

That is weak positioning.

Not because you need to become an accountant. You do not. But because financial blindness makes you slower, more reactive, and more dependent on others to tell you if your business is working.

The business owners who win are not necessarily the ones with the most sophisticated accounting systems. They are the ones who understand the handful of concepts that matter. They ask better questions. They recognize when something is off before it becomes a crisis.

This article is that handful of concepts.

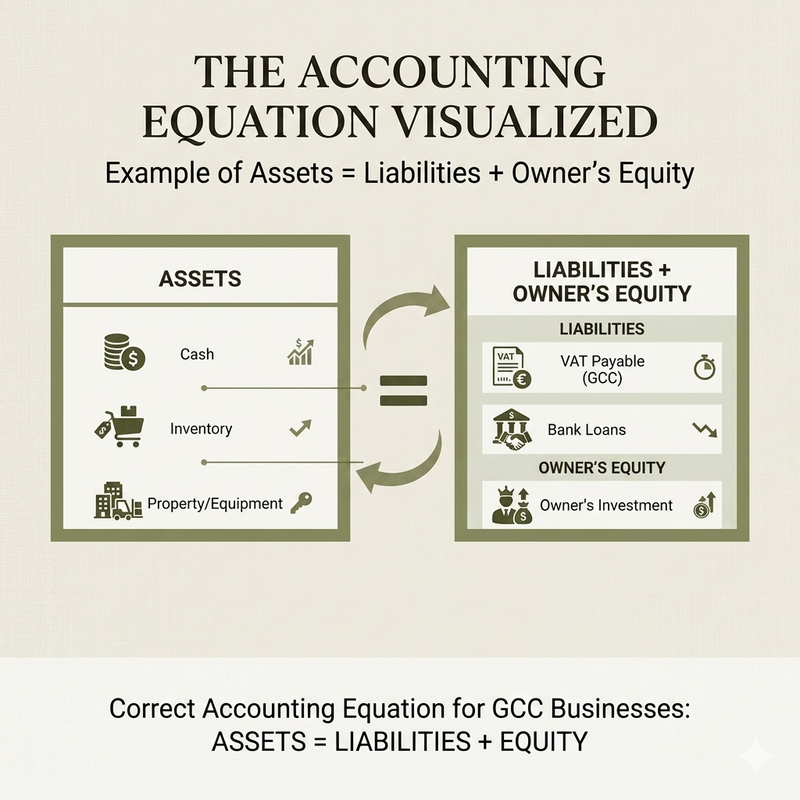

The One Equation That Runs Your Business

Everything in accounting software revolves around one unbreakable equation. If this equation does not balance, the system has a problem.

Assets = Liabilities + Equity

Here is what that actually means:

Assets: What your company owns. Cash in the bank, money customers owe you (accounts receivable), inventory, equipment, software subscriptions you prepaid.

Liabilities: What your company owes. Bills from suppliers (accounts payable), loans, VAT you collected but have not paid yet, employee salaries you owe.

Equity: What is left over for the owners. If you sold everything and paid off all debts, this is what you would walk away with.

The equation is not a philosophy. It is the structure of the system.

When you make a sale, both sides of the equation change. Cash goes up (asset increases). Equity goes up because you made a profit (retained earnings). When you take a loan, cash goes up (asset) and debt goes up (liability). The equation stays balanced.

In the GCC, this equation carries extra weight because of VAT. When you collect 100 SAR from a customer and 5 SAR of that is VAT, the 5 SAR does not belong to you. It is a liability. Your accounting system tracks this so you do not accidentally spend money that belongs to the tax authority.

That is why ZATCA e-invoicing and Fatoora compliance matter. The invoice is not just a receipt. It is the transaction that moves the equation.

Debits and Credits: The Language Your Accountant Speaks

If you have ever heard an accountant say "debit the asset account and credit the revenue account," and felt lost, here is the translation.

Debits and credits are the language of double-entry accounting. Every transaction affects at least two accounts. One gets debited, one gets credited. The sum of debits must equal the sum of credits.

You do not need to memorize this table.

What you need to know is that the system requires balance. If your accountant says "the books do not balance," this is what they mean. The debits and credits do not add up. Something was recorded incorrectly.

Modern accounting software handles this automatically. You do not manually debit and credit accounts. But when your accountant explains why a transaction was recorded a certain way, this is the framework they are working within.

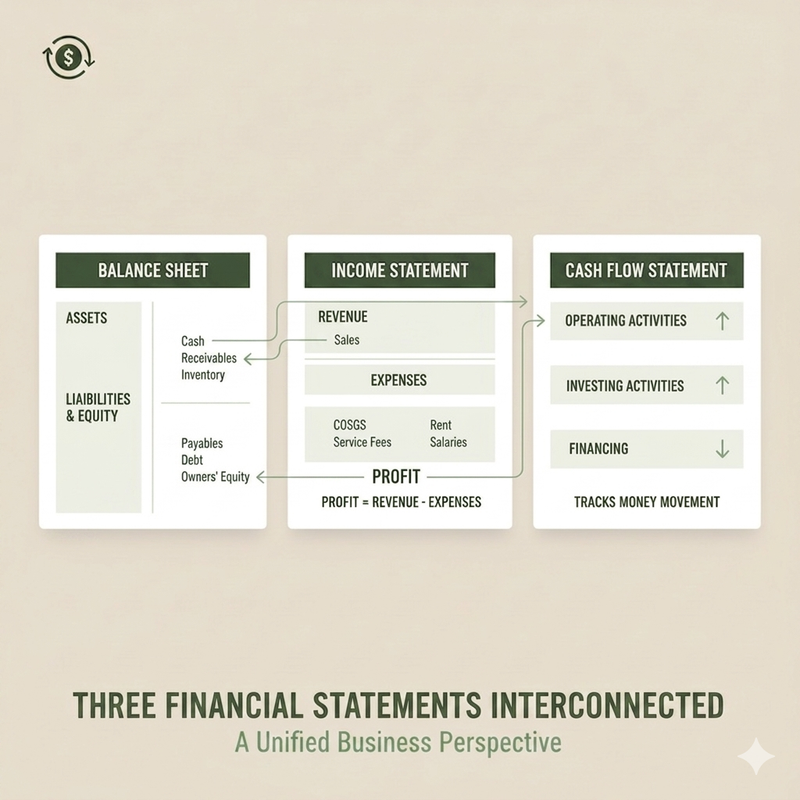

The Three Reports That Tell You If Your Business Is Working

Your accounting system exists to produce three reports. These are the output of all the data entry, all the reconciliations, all the journal entries.

If you understand these three reports, you understand your business.

Balance Sheet: The Snapshot

The balance sheet shows your financial position at a specific moment in time. It is a freeze-frame.

On one side: everything you own (assets). On the other side: everything you owe (liabilities) plus what is left for the owners (equity).

Assets = Liabilities + Equity. The equation proves itself here.

GCC examples:

- Assets: Cash in your bank account, money a customer in Riyadh owes you for an invoice (accounts receivable), inventory sitting in your warehouse, a delivery van you purchased last year.

- Liabilities: A bill from your supplier in Dubai you have not paid yet (accounts payable), a bank loan for equipment, VAT you collected this month but have not remitted to ZATCA.

- Equity: The initial capital you invested when you started the business, plus all the profit you have retained over the years.

The balance sheet does not tell you how the business performed this month. It tells you where you stand right now.

Income Statement: The Performance Report

The income statement (also called a profit and loss statement or P&L) shows performance over a period of time. A month, a quarter, a year.

Revenue - Expenses = Net Income (Profit or Loss)

This is the report that tells you if the business is making money.

But there is a layer most business owners miss. Not all profit is created equal.

Gross Profit = Revenue - Cost of Goods Sold (COGS)

This tells you if the core product is priced correctly. If you sell a product for 1,000 SAR and it costs you 800 SAR to make or buy, your gross profit is 200 SAR. If gross profit is low or negative, you have a pricing problem or a cost problem. Everything else is secondary.

EBITDA (or Operating Profit) = Gross Profit - Operating Expenses

This is what investors and lenders look at. It strips away things you do not control (taxes, interest, depreciation) and shows how the actual business engine is running. Strong EBITDA means the core operations generate cash.

EBIT = EBITDA - Depreciation & Amortization

This accounts for the fact that equipment and software wear out over time and will need to be replaced. It is a more conservative view of profitability.

Net Income = EBIT - Interest - Taxes - Other Income/Expenses

This is the bottom line. What is left after everything.

Why does this matter? Because a business can have strong revenue but weak gross profit. Or strong gross profit but terrible operating expenses. The layers tell you where the problem is.

Cash Flow Statement: The Reality Check

A business can be profitable on paper and still run out of cash.

The income statement tells you if you made a profit. The cash flow statement tells you if you actually have the money.

Example: You sell a 50,000 SAR project to a client in Dubai. You record the revenue today (accrual accounting). But the client has 30-day payment terms. You made a profit on paper. You do not have the cash yet.

Meanwhile, you have to pay your team salaries, pay your supplier invoices, pay rent. If your cash flow is negative, you have a problem even though you are technically profitable.

This is why e-invoicing and tight accounts receivable management matter in the GCC. The faster you get paid, the healthier your cash flow.

Cash vs Accrual: When Does a Sale Actually Count?

There are two ways to record transactions: cash basis and accrual basis.

Cash Basis: You record a sale when the money hits your bank account. Simple. Like a personal checkbook.

Accrual Basis: You record a sale when you provide the service or ship the product, even if the customer has not paid you yet.

Most GCC businesses over a certain size are required to use accrual accounting. Why? Because it gives a more accurate picture of financial health.

Under cash accounting, you could have a massive sale in December that does not show up until January when the payment arrives. Your December financials would look weak even though you crushed the month. Accrual accounting fixes that.

The trade-off: accrual accounting is more complex. You have to track receivables (money you are owed) and payables (money you owe) separately from actual cash. Modern accounting software handles this automatically, but it is why you cannot just look at your bank balance and know if you are profitable.

The Terms You Will Hear in Every Finance Meeting

General Ledger: The master record. It is the complete log of every financial transaction your business has ever made. When someone says "close the books," they mean lock the general ledger so no more changes can be made for that period.

Chart of Accounts: The filing system. Every transaction gets filed into a specific account. "Office Supplies." "Travel Expenses." "Sales Revenue." If the chart of accounts is messy, the reports will be meaningless.

Accounts Receivable (AR): Money customers owe you. Think of it as money waiting to be received. If your AR is growing faster than your revenue, you have a collections problem.

Accounts Payable (AP): Money you owe suppliers or vendors. Bills that need to be paid. If your AP is growing too fast, you might be stretching payment terms too thin.

Reconciliation: The process of cross-referencing your accounting records against your bank statements to make sure they match. If the bank says you have 10,000 SAR and your books say 9,500 SAR, you have a discrepancy. Find it.

Depreciation: How businesses spread the cost of an expensive asset (like a laptop or a delivery truck) over its useful life instead of taking the whole expense the day they buy it. It is a non-cash expense (you are not actually spending money this month), but it impacts profitability.

Trial Balance: A report that lists the balances of all general ledger accounts. Its purpose is to prove that Total Debits = Total Credits. If they do not match, the books are out of balance. Something was recorded wrong.

Fiscal Year: The one-year period a company uses for financial reporting. Not always January to December. Some GCC companies align their fiscal year with Hijri calendar cycles or use April-March to match regional business cycles.

What This Means for You

You are not going to become an accountant after reading this.

That is not the point.

The point is that you can now sit in a meeting with your CFO or your accountant and understand what they are talking about. You can ask better questions. You can spot when something does not add up.

Three questions every business owner should ask their accountant every month:

What is our cash runway? (How many months can we operate at current burn rate before we run out of cash?)

What is our gross profit margin this month vs last month? (Is the core business getting stronger or weaker?)

How many days is our average accounts receivable outstanding? (How long does it take to collect payment from customers?)

These three questions tell you more about the health of your business than staring at the bottom line of the income statement.

Modern accounting software like Bizrah handles the mechanics automatically. The debits and credits. The reconciliations. The trial balance. You do not need to worry about whether the equation balances. The software does that.

What you need to focus on is the insights. The trends. The warning signs.

That is the difference between running a business and running it blind.

See how Bizrah automates the accounting mechanics while keeping you in control of the insights → Start your free trial