General Ledger vs Trial Balance: Key Differences Explained

General Ledger vs Trial Balance: Key Differences Explained

The general ledger is the source. The trial balance is the check.

Business owners hear both terms in every accounting conversation. But most cannot explain the difference.

That creates a problem when your accountant asks you to review the trial balance, and you open the general ledger instead. Or when you try to find a specific transaction in your trial balance and realize it is not there.

These are two different tools that serve two different purposes. Using one when you need the other wastes time.

The Short Answer

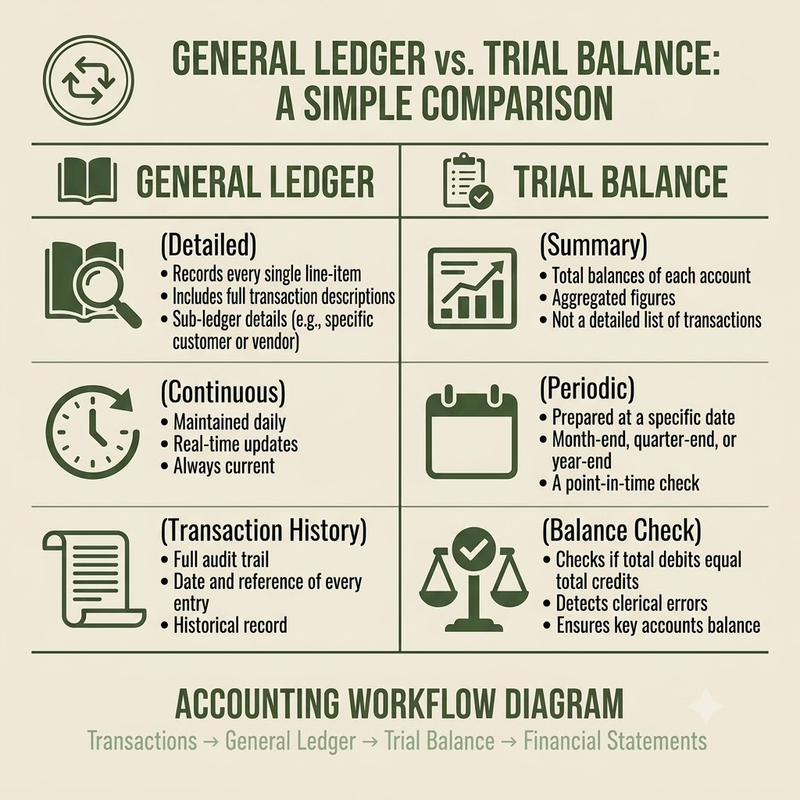

The general ledger records every transaction your business makes. It is the master record. Every sale, every purchase, every payment, every adjustment lives in the general ledger.

The trial balance is a snapshot of all account balances at a single point in time. It lists every account and checks that debits equal credits. It catches mathematical errors. It does not show individual transactions.

If you need to know what happened, check the general ledger. If you need to verify your books balance, check the trial balance.

For more on basic accounting concepts, read our accounting for non-accountants guide.

What the General Ledger Actually Is

The general ledger is a complete record of all financial transactions, organized by account.

Think of it as a collection of individual account ledgers. One ledger for cash. One for accounts receivable. One for rent expense. One for revenue. Each account shows every transaction that affected it.

Real-world example:

You sell 10,000 SAR worth of goods to a customer on credit. The entry is:

Date: 2026-05-15

Debit: Accounts Receivable 10,000 SAR

Credit: Sales Revenue 10,000 SAR

This transaction appears in two places in the general ledger:

1. The Accounts Receivable ledger shows a 10,000 SAR debit on 2026-05-15

2. The Sales Revenue ledger shows a 10,000 SAR credit on 2026-05-15

Two weeks later, the customer pays. Another entry:

Date: 2026-05-29

Debit: Cash 10,000 SAR

Credit: Accounts Receivable 10,000 SAR

Now the Cash ledger shows a 10,000 SAR debit. The Accounts Receivable ledger shows a 10,000 SAR credit that offsets the earlier debit.

Every transaction flows through the general ledger this way. If you want to understand why your cash balance is what it is, you open the cash account in the GL and see every deposit and withdrawal.

The general ledger is continuous. It does not reset. It builds from the first day you opened your business to today.

What the Trial Balance Actually Is

The trial balance is a list of all accounts and their current balances at a specific date. It does not show transactions. It shows ending balances.

The format is simple: two columns. Debit balances on the left. Credit balances on the right.

Real-world example (Trial Balance as of 2026-05-31):

The totals match. That means the books balance. Every debit has a corresponding credit. This is the fundamental rule of double-entry bookkeeping.

If the totals do not match, there is an error. Either a transaction was posted with unequal debits and credits, or a number was entered wrong. The trial balance catches this immediately.

But notice what the trial balance does not show: how you arrived at these balances. It does not show that cash balance came from 15 deposits and 8 withdrawals. It just shows the ending balance.

The Key Differences

The general ledger is the detail. The trial balance is the summary check.

Purpose: The general ledger records all transactions in detail. The trial balance verifies that debits equal credits.

When: The general ledger is continuous, with every transaction posted immediately. The trial balance is periodic, usually monthly or quarterly.

Detail level: The general ledger provides a full transaction history with dates, descriptions, and references. The trial balance offers summary balances only.

Output: The general ledger shows individual account activity. The trial balance lists all accounts with ending balances.

Errors caught: The general ledger is the source of truth. The trial balance catches mathematical errors (debit/credit imbalance).

Use case: Use the general ledger to investigate specific transactions or account activity. Use the trial balance to verify accounting accuracy before preparing financial statements.

What the Trial Balance Cannot Catch

A balanced trial balance means your debits equal your credits. That is all it means.

It does not mean your books are error-free.

Common Errors That Slip Through

1. Posting to the wrong account:

You record rent expense as salaries expense. Both are expense accounts. The entry still balances. The trial balance looks fine. But your rent expense is understated and salaries expense is overstated.

2. Missing transactions:

You forget to record a 5,000 SAR sale. No entry was made. There is nothing to unbalance the trial balance. Your revenue is understated by 5,000 SAR. The trial balance does not know.

3. Duplicate entries:

You record the same 10,000 SAR supplier payment twice. Both entries balance. The trial balance shows nothing wrong. But your cash is understated by 10,000 SAR and your accounts payable is understated by 10,000 SAR.

4. Offsetting errors:

You overstate revenue by 2,000 SAR and overstate expenses by 2,000 SAR. The net effect on your balance sheet is zero. The trial balance balances. But your profit is wrong.

5. Errors in original amounts:

You enter 15,000 SAR instead of 1,500 SAR. The entry balances (debit and credit both use 15,000 SAR). The trial balance is fine. But the amount is wrong.

This is why a balanced trial balance is necessary but not sufficient. You still need account reconciliations, reviews, and controls to catch these errors.

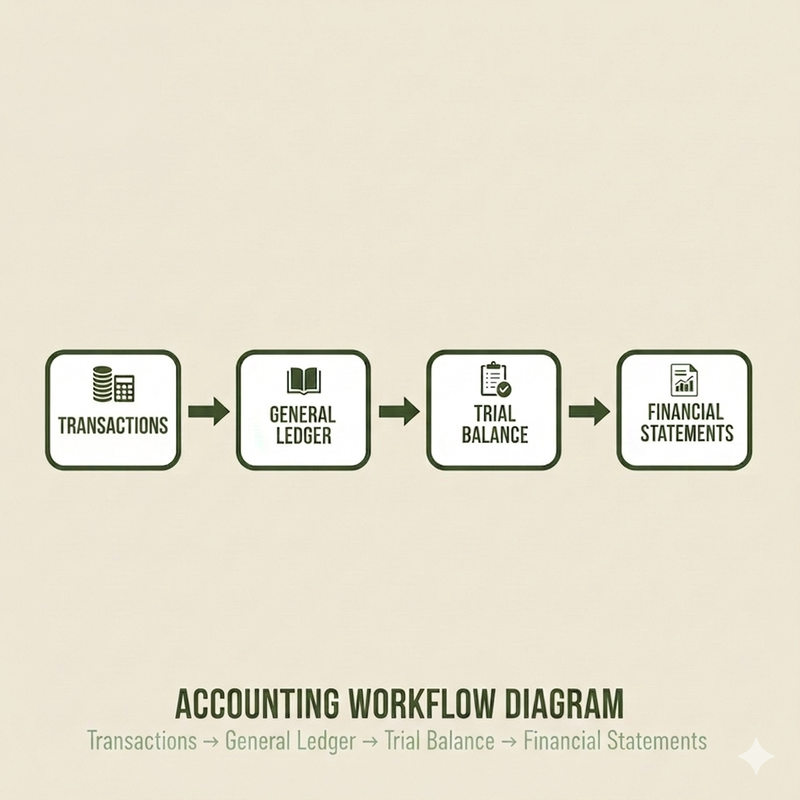

The Workflow: From GL to Financial Statements

Every business follows this sequence:

1. Transactions → General Ledger

As transactions happen, you post them to the GL. This happens daily (or in real-time with cloud accounting systems).

2. General Ledger → Trial Balance

At period-end (monthly or quarterly), you generate a trial balance. This summarizes all GL account balances.

3. Trial Balance → Adjusting Entries

You review the trial balance and make adjusting entries (accruals, deferrals, depreciation, corrections). These entries are posted back to the GL.

4. Adjusted Trial Balance

After adjustments, you generate a new trial balance. This is the adjusted trial balance. It includes all corrections.

5. Adjusted Trial Balance → Financial Statements

From the adjusted trial balance, you prepare:

- Income statement (revenue and expense accounts)

- Balance sheet (asset, liability, and equity accounts)

- Cash flow statement (derived from changes in balance sheet accounts and income statement)

The trial balance is the bridge between your detailed GL and your summary financial statements.

If you skip the trial balance and go straight from GL to financial statements, you risk publishing statements with unbalanced accounts. That breaks everything downstream.

Practical Tips for GCC SMEs

How often should you review your GL?

Weekly if you are hands-on with your finances. Monthly at minimum. Look for unusual transactions, duplicate entries, accounts that should not have activity.

How often should you run a trial balance?

Monthly, before you close your books for the month. Some businesses run it weekly as an early warning system.

Red flags in your trial balance:

- Suspense accounts with balances (these should be cleared regularly)

- Negative balances in accounts that should never be negative (e.g., negative cash, negative inventory)

- Unallocated or "other" accounts with large balances

- Balance sheet accounts with balances that do not make sense (e.g., prepaid expenses from five years ago)

What to do if your trial balance does not balance:

1. Recalculate the totals (sounds obvious, but sometimes it is a sum error)

2. Check for transposed numbers (1,500 entered as 15,000)

3. Review recent journal entries for missing debits or credits

4. Check for entries posted only to one side of the ledger

5. If your accounting software allows unbalanced entries, search for them

How automated systems handle this:

Modern cloud accounting systems like Bizrah do not allow you to post an unbalanced entry. If you try to debit 10,000 SAR and credit 9,000 SAR, the system rejects it. This prevents most trial balance errors before they happen.

The GL and TB are auto-generated in real-time. You do not manually compile them. This removes the risk of calculation errors and ensures your trial balance is always current.

The Bottom Line

The general ledger is your transaction history. The trial balance is your balance check.

You need both. But they are not interchangeable.

When you want to understand why an account balance is what it is, open the general ledger for that account. When you want to verify your books are mathematically sound before preparing financial statements, run a trial balance.

Most accounting software generates both automatically. You do not manually maintain them. But you do need to understand what they show and what they do not show.

A trial balance that balances is good. A trial balance that balances and has been reconciled and reviewed is better. The former means your math is right. The latter means your accounting is right.

Bizrah auto-generates your general ledger and trial balance in real-time. Start your free trial