Cash vs. Accrual Accounting: Make the Right Choice for Your Business

Cash vs. Accrual Accounting: Make the Right Choice for Your Business

Most businesses pick an accounting method by accident. That choice shapes every financial decision you make.

Why This Choice Matters More Than Most Business Owners Think

You probably did not sit down and decide which accounting method to use.

You started recording transactions the way that felt natural. Revenue went in when the bank account moved. Expenses went out when you paid the bill. That is cash basis accounting, and for many early-stage businesses, it happens by default.

But here is the problem: the accounting method you choose affects cash flow visibility, tax filing accuracy, and your ability to scale. In the GCC, regulatory requirements can force the choice on you whether you are ready or not.

This is not an abstract accounting question. It is a systems decision. The wrong method creates blind spots. The right one gives you a true picture of your business.

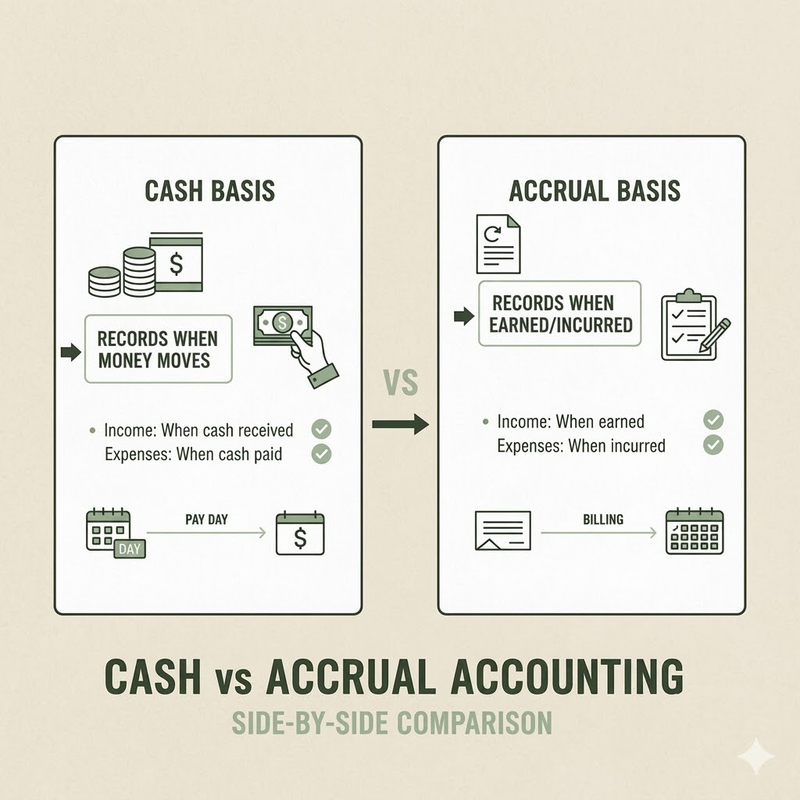

What Cash Basis Accounting Actually Means

Cash basis accounting records revenue when cash hits the bank and expenses when you pay them. That is it.

If a client pays you today, that is revenue today. If you pay a supplier next month, that is an expense next month. The timing is tied entirely to cash movement.

Who uses it: Freelancers, micro-businesses, service companies with no inventory, and businesses that get paid immediately.

The advantage: It is simple. It matches your bank statements. It shows your real cash position at any moment. You do not need to track receivables or payables. You do not need complex reconciliations.

The weakness: It hides future obligations. If you invoiced a client in March but they pay in April, March looks terrible and April looks great. Neither month reflects what actually happened. You cannot match revenue to the work that generated it. You cannot see profitability by project or client accurately.

In the GCC, most sole proprietorships and small shops default to cash basis because it is easy and regulatory requirements do not force them to switch.

What Accrual Accounting Actually Means

Accrual accounting records revenue when you earn it and expenses when you incur them, not when cash moves.

If you deliver a project in March and invoice the client, that is March revenue, even if they pay in April. If you receive supplies in February and get the bill in March, that is a February expense.

Who uses it: Growing SMEs, inventory-based businesses, companies with credit terms, and businesses that need accurate project-level profitability.

The advantage: It shows true profitability. It matches revenue to the work that generated it. It gives you accurate gross margins. It helps you track performance by project, client, or product line. It is the foundation for serious financial planning.

The weakness: It is more complex. It requires discipline. You have to track receivables and payables. You can show a profit on paper but have no cash in the bank. That gap between profit and cash confuses many business owners.

In the GCC, many jurisdictions mandate accrual accounting for companies over a certain size, for entities with inventory, or for businesses that file corporate tax returns. You do not always get to choose.

The Real Question Is Not Which Is "Better"

Stop asking which method is better. Ask which fits your business model.

Matching Method to Business Model

Cash basis works if:

- You get paid immediately or within a few days

- You have no inventory

- You do not offer credit terms to clients

- You are a solo operator or micro-business

- Your jurisdiction does not require accrual

Accrual works if:

- You invoice clients on 30-day or 60-day terms

- You carry inventory

- You track project costs and need accurate margins

- You have employees and complex cost structures

- You are planning to raise capital or sell the business

The mistake many businesses make is outgrowing cash basis and not switching. You start offering credit terms, but you are still on cash basis. Suddenly your financial reports no longer make sense. March shows zero revenue because no one paid yet, even though you delivered three projects. That is a blind spot.

If you are still figuring out whether accounting matters for your business at all, read our guide on whether small businesses need accounting.

When GCC Regulations Force the Decision

In many GCC markets, the law decides for you.

UAE: The Federal Tax Authority's corporate tax rules may require accrual accounting for certain entity types, especially companies with revenue over specific thresholds or businesses filing audited financials.

Saudi Arabia: ZATCA and SOCPA (Saudi Organization for Chartered and Professional Accountants) standards push medium and larger businesses toward accrual. If you are a limited liability company or planning to grow beyond a small operation, accrual is the expected standard.

Egypt: Accrual is the standard for registered companies. Cash basis is limited to very small businesses and freelancers.

Bahrain, Kuwait, Oman, Qatar: Similar patterns. As businesses formalize, accrual becomes mandatory or strongly preferred.

The key insight: do not wait for a compliance deadline to switch. The transition takes time, planning, and clean historical data. If you know you will need to switch in two years, start now while your data set is still manageable.

The Switching Cost People Underestimate

Switching from cash to accrual mid-year creates reconciliation headaches. Your historical comparisons break. Year one is on cash basis, year two is on accrual. Those numbers are not comparable. You cannot trend them. You cannot use them to forecast.

If you switch in the middle of a fiscal year, you end up with partial data on two different methods. That confuses investors, banks, and auditors.

The advice: If you are growing and you see the switch coming, do it early while your data set is still small. Pick a fiscal year-end, make the switch clean, and do not straddle.

Switching also means training your team (or yourself) on new concepts: accounts receivable, accounts payable, deferred revenue, accrued expenses. If you have been on cash basis for years, those concepts feel abstract until you start using them every day.

The longer you wait, the messier it gets.

What to Do Next

Here is how to decide:

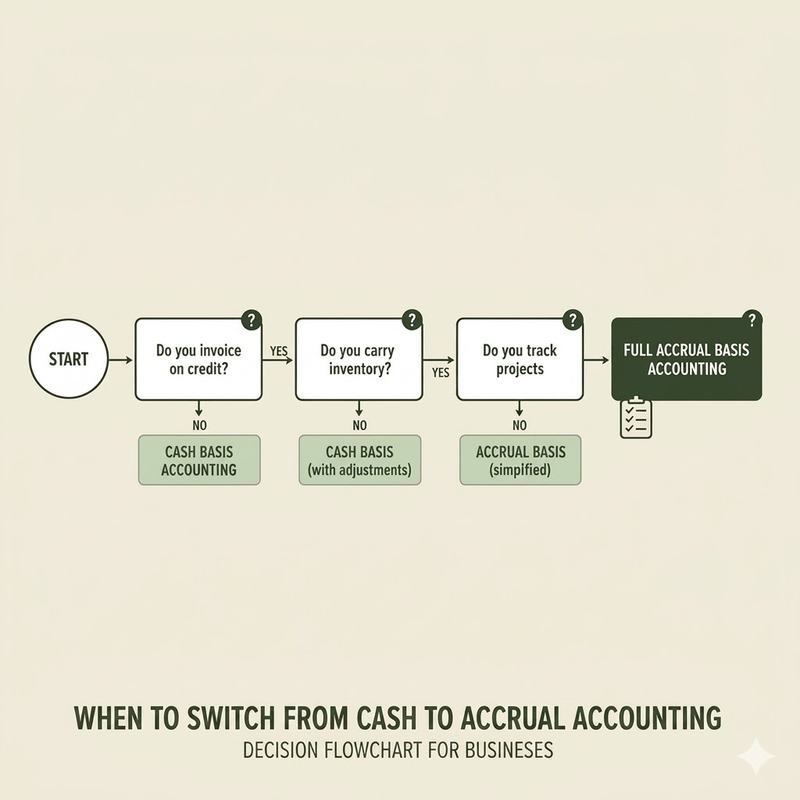

Step 1: Audit your business model. Do you invoice on credit? Do you carry inventory? Do you need accurate project profitability? If yes to any of these, you likely need accrual.

Step 2: Check GCC regulatory requirements for your entity type and jurisdiction. If you are incorporated, if you file corporate tax, or if you are above certain revenue thresholds, accrual may already be required.

Step 3: If you are on cash basis and experiencing blind spots (late invoices distorting your income, inventory confusion, inaccurate margins), plan the switch. Do not wait for a crisis or a compliance deadline.

Step 4: Use software that handles both methods. Do not let your accounting method lock you in. The right platform lets you switch cleanly and keeps historical data intact.

This is not a one-time decision. As your business grows, the method that worked at 10 transactions per month stops working at 500. Plan the transition before it becomes urgent.

For more foundational accounting concepts, see our complete guide to accounting for non-accountants.

See how Bizrah handles both cash and accrual accounting for GCC businesses → Try Bizrah free for 14 days