Foreign Exchange Risk Management: Types & Strategies for GCC Businesses

Foreign Exchange Risk Management: Types & Strategies for GCC Businesses

Currency fluctuations can quietly erode profit margins. Here is how to identify your exposure and manage it without building a treasury department.

Most GCC business owners do not think about foreign exchange risk until they take a loss. A supplier in China raises prices unexpectedly. A payment to a US vendor costs 8 percent more than budgeted. A quarterly financial statement shows an unrealized FX loss that wipes out half the operating profit.

By then, the damage is done.

Foreign exchange risk is not just for multinational corporations with dedicated treasury teams. If you import goods, pay foreign suppliers, or compete with companies that benefit from favorable exchange rates, you have exposure. The question is whether you are managing it or ignoring it.

This guide explains the three types of FX risk every business faces, the strategies you can use to manage them, and when hedging makes sense for your situation.

What is Foreign Exchange Risk?

Foreign exchange risk is the possibility that currency fluctuations will negatively impact your business finances.

It shows up in three ways: when exchange rates change between the time you agree to a transaction and the time you settle it, when you consolidate financial statements across multiple currencies, and when sustained currency movements shift your competitive position over time.

Why It Matters for GCC Businesses

Most GCC currencies are pegged to the US dollar. The Saudi riyal, UAE dirham, Bahraini dinar, Omani rial, and Qatari riyal maintain fixed exchange rates against the dollar. The Kuwaiti dinar is pegged to a basket of currencies, but the dollar dominates that basket.

This peg creates a false sense of security. Yes, your local currency is stable against the dollar. But if you pay suppliers in euros, yuan, or pounds, you still have exposure. If you compete with Turkish or Egyptian companies whose currencies have depreciated significantly, your pricing becomes less competitive even though your costs have not changed.

Currency risk is real even when your home currency is pegged.

Real Example: UAE Company Paying a US Supplier

A Dubai-based retailer orders $100,000 worth of inventory from a US supplier. The supplier offers 90-day payment terms. At the time of the order, the exchange rate is stable because the dirham is pegged to the dollar.

But the retailer also sources packaging materials from a European supplier and pays in euros. When the order is placed, the euro-to-dirham rate is 4.05. By the time payment is due 90 days later, the euro has strengthened to 4.20.

The $10,000 invoice that was supposed to cost AED 40,500 now costs AED 42,000. The retailer just lost AED 1,500 without any change in the product, the supplier, or the business fundamentals.

That is transaction risk.

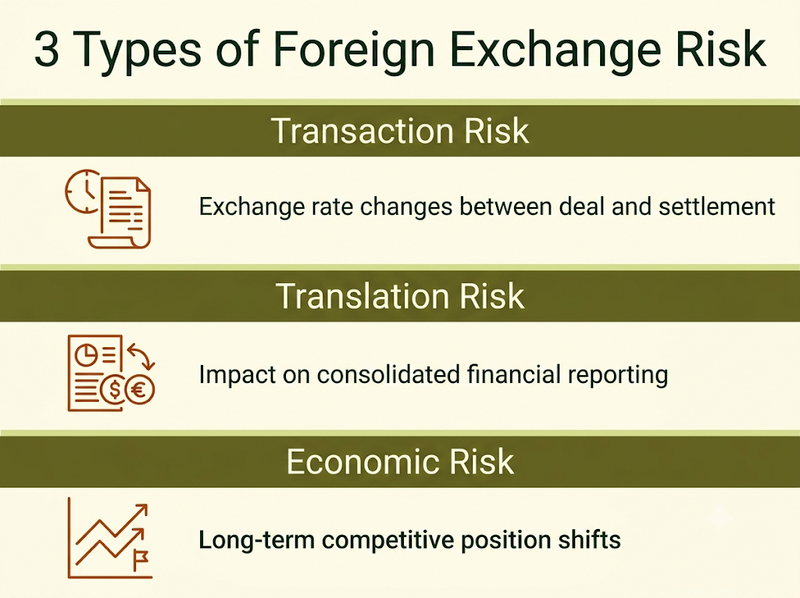

The Three Types of FX Risk Every Business Faces

Foreign exchange risk is not one thing. It shows up in different forms depending on how your business interacts with foreign currencies.

Transaction Risk

Transaction risk is the impact of exchange rate changes on specific transactions between the time you commit to a deal and the time cash changes hands.

When it hits: Between order placement and payment settlement. The longer the payment cycle, the greater the exposure.

Who is affected: Importers, exporters, and any company paying or receiving foreign currency for goods or services.

Example: A Saudi company orders manufacturing equipment from Germany. The invoice is EUR 50,000. At the time of order, the exchange rate is SAR 1 = EUR 0.24, so the expected cost is SAR 208,333. Three months later, when payment is due, the euro has strengthened to SAR 1 = EUR 0.22. The actual cost is now SAR 227,272. The company just paid SAR 18,939 more than planned.

Transaction risk is the most visible and immediate form of FX exposure. It is also the easiest to quantify and hedge.

Translation Risk (Accounting Risk)

Translation risk is the impact of exchange rate changes on consolidated financial statements when you operate in multiple currencies.

When it hits: During quarterly or annual financial reporting when you convert foreign subsidiary financials into your home currency.

Who is affected: Multi-country businesses, parent companies with foreign subsidiaries, and any business that reports consolidated financials across currencies.

Example: A Saudi parent company owns a subsidiary in the UAE. The subsidiary earns AED 1 million in profit. At the beginning of the year, the exchange rate is SAR 1 = AED 0.98. The subsidiary's profit translates to SAR 1,020,408 on the consolidated income statement.

By year-end, the dirham weakens slightly to SAR 1 = AED 1.02. The same AED 1 million now translates to SAR 980,392. The consolidated financials show a SAR 40,016 loss purely from currency translation, even though the subsidiary's actual operations were unchanged.

Translation risk does not affect cash flow immediately, but it distorts reported earnings and can trigger covenant violations in debt agreements or alarm investors who do not understand that the underlying business is healthy.

Economic Risk (Operating Risk)

Economic risk is the long-term impact of sustained currency movements on your competitive position and operating margins.

When it hits: Over months or years as exchange rates shift and change the relative cost structure of competitors or the purchasing power of your customer base.

Who is affected: Export-heavy businesses, companies competing with imports, and businesses whose customers earn income in foreign currencies.

Example: An Egyptian software company sells services priced in US dollars to GCC clients. Over two years, the Egyptian pound depreciates 40 percent against the dollar. The company's local costs (salaries, rent, utilities) are now 40 percent cheaper in dollar terms. It can undercut Saudi competitors on price while maintaining the same profit margins.

Saudi competitors face a choice: match the lower prices and accept margin compression, or lose market share. Neither option is caused by their own performance. The currency movement changed the playing field.

Economic risk is the hardest to quantify and the slowest to recognize. By the time you notice it, competitors have already gained ground.

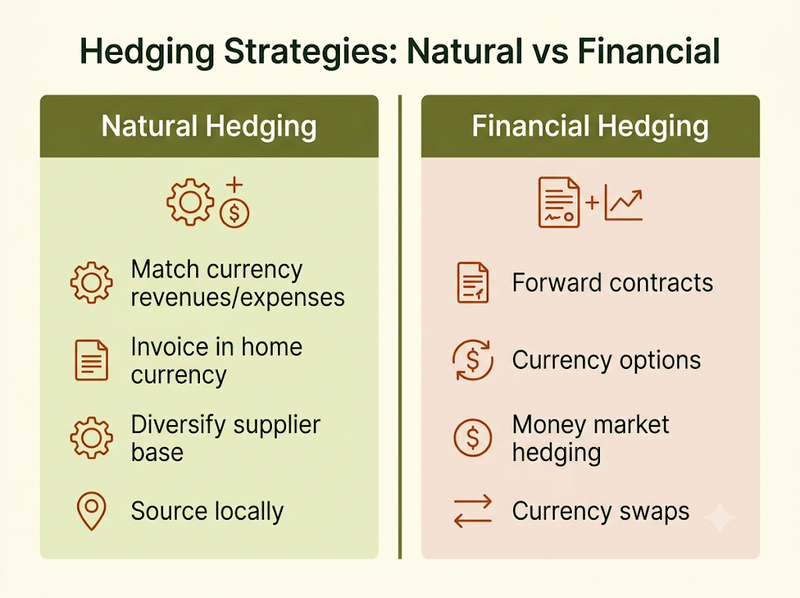

Natural vs. Financial Hedging Strategies

Hedging means reducing your exposure to currency risk. There are two broad approaches: natural hedging (operational adjustments) and financial hedging (using financial instruments).

Natural Hedging (Operational Strategies)

Natural hedging is restructuring your operations so revenues and expenses in the same currency offset each other. No derivatives, no banks, no complex instruments.

Match Currency Revenues and Expenses

If you earn euros, try to pay suppliers in euros. If you earn dollars, source from dollar-denominated suppliers.

This is the simplest and most effective form of hedging. When revenues and costs move in the same direction, exchange rate changes cancel out.

Example: A UAE logistics company earns 60 percent of its revenue in euros from European clients. Instead of converting euros to dirhams and then paying suppliers in dollars, the company sources fuel and vehicle leases from European providers and pays them directly in euros. Currency fluctuations no longer impact margins on the European side of the business.

Pros: No transaction costs, no counterparty risk, no complexity.

Cons: Not always feasible. You may not have euro-denominated suppliers in your market, or euro suppliers may be more expensive than alternatives.

Invoice in Your Home Currency

Pass the FX risk to the customer by pricing everything in your local currency.

Example: A Saudi consulting firm invoices all clients in Saudi riyals, regardless of where the client is based. If a European client wants to pay, they convert euros to riyals. The consulting firm never touches foreign currency.

Pros: Zero FX risk for you.

Cons: You may lose deals if clients are unwilling to accept the risk. Large clients with their own treasury operations will push back. Smaller clients may simply choose a competitor who invoices in their currency.

Diversify Your Supplier and Customer Base

If you rely on a single currency for a large portion of revenue or expenses, a sudden movement in that currency creates concentrated risk. Spreading exposure across multiple currencies reduces the impact of any single rate change.

Example: A Qatar-based retailer sources products from China (yuan), Turkey (lira), and India (rupee). When the yuan strengthens 10 percent, it only affects one-third of the cost base. The overall margin impact is diluted.

Pros: Reduces concentration risk.

Cons: Managing multiple supplier relationships and payment currencies adds operational complexity.

Source Locally When Feasible

Buy from domestic suppliers to eliminate FX exposure entirely.

Pros: No currency risk, shorter supply chains, faster delivery.

Cons: Local suppliers may be more expensive or offer lower quality. The cost savings from avoiding FX risk may not offset the higher purchase price.

Financial Hedging (Using Financial Instruments)

Financial hedging uses contracts to lock in exchange rates or limit downside risk. These instruments are widely available through commercial banks in the GCC, but they come with costs and complexity.

Forward Contracts

A forward contract locks in an exchange rate for a future date. You agree today to exchange a specific amount of currency at a specific rate on a specific date, regardless of what the market rate is at that time.

Example: A Saudi company knows it will pay EUR 100,000 to a supplier in six months. It enters a forward contract with a bank to buy EUR 100,000 at SAR 1 = EUR 0.23, locking in a cost of SAR 434,782. If the euro strengthens to SAR 1 = EUR 0.21 by payment date, the company still pays SAR 434,782. It avoided a loss. If the euro weakens to SAR 1 = EUR 0.25, the company still pays SAR 434,782. It gave up the potential gain in exchange for certainty.

Best for: Predictable, scheduled payments where you value certainty over upside potential.

Pros: Simple, widely available, no upfront premium.

Cons: You are locked in. If the exchange rate moves in your favor, you cannot benefit.

Currency Options

A currency option gives you the right, but not the obligation, to exchange currency at a set rate on or before a specific date. You pay an upfront premium for this flexibility.

Example: The same Saudi company buys a call option giving it the right to buy EUR 100,000 at SAR 1 = EUR 0.23. The premium costs SAR 5,000. If the euro strengthens to SAR 1 = EUR 0.21, the company exercises the option and saves money. If the euro weakens to SAR 1 = EUR 0.25, the company lets the option expire and buys euros at the favorable market rate. The company is protected against downside but can still benefit from upside.

Best for: Transactions where you are uncertain whether the payment will happen (pending contract approval, regulatory clearance, etc.).

Pros: Downside protection with upside flexibility.

Cons: The upfront premium can be expensive. If the rate does not move much, you lose the premium and gain nothing.

Money Market Hedging

Money market hedging involves borrowing in the foreign currency, converting it to your home currency immediately, and investing it until the payment is due. At payment time, you use the matured investment to pay the liability.

Example: A UAE company owes EUR 100,000 in six months. It borrows EUR 95,000 today (the present value of EUR 100,000 in six months), converts it to dirhams at the current spot rate, and invests the dirhams in a short-term deposit. In six months, the euro loan comes due. The company uses the matured dirham deposit to buy euros and repay the loan. The effective exchange rate was locked in at the time of the initial conversion.

Best for: Larger companies with access to credit and short-term investment options.

Pros: Can be cheaper than forward contracts if borrowing rates are favorable.

Cons: Requires credit facilities in multiple currencies. More complex to execute and manage.

Currency Swaps

A currency swap is an agreement to exchange principal and interest payments in one currency for principal and interest payments in another currency. It is typically used for long-term exposures, such as foreign debt or multi-year contracts.

Example: A Saudi company issues a euro-denominated bond to finance European expansion. It enters a currency swap to convert euro interest payments into riyal payments. The company effectively borrows in riyals even though the bond is euro-denominated.

Best for: Long-term, recurring exposures (multi-year debt, long-term supplier contracts, foreign subsidiary operations).

Pros: Matches long-term cash flows and eliminates ongoing FX risk.

Cons: Complex, expensive, and requires counterparties willing to take the opposite side of the swap.

When to Hedge (And When Not To)

Hedging is not free. Forward contracts tie up credit lines. Options cost premium. Money market hedges require treasury infrastructure. You need to decide whether the cost of hedging is justified by the risk you are eliminating.

Assess Your Exposure

Start by quantifying how much of your revenue and expenses are in foreign currencies.

If 80 percent of your costs are local and 90 percent of your revenue is local, your FX exposure is minimal. A 10 percent currency swing might affect 2 to 3 percent of your total cost base. That is noise, not a material risk.

If 60 percent of your costs are in foreign currencies and payment cycles are 90 days or longer, a 5 percent currency move can wipe out your operating margin. That is material. That is worth hedging.

Materiality Threshold

Would a 10 percent currency move change the outcome of a business decision? If yes, hedge. If no, accept the risk.

Example: A company imports goods with a 5 percent net margin. A 5 percent unfavorable currency move turns a profitable transaction into a break-even or loss. This company should hedge.

Another company has 20 percent margins and only 15 percent of costs are foreign-denominated. A 5 percent currency move reduces margins to 19.25 percent. The business is still healthy. Hedging may not be worth the cost.

Cost of Hedging vs. Potential Loss

Forward contracts and options are not free. Banks charge spreads. Option premiums can be 2 to 3 percent of the notional amount. If your potential FX loss is 3 percent and the hedge costs 2.5 percent, you are paying almost as much to hedge as the loss you are avoiding.

Hedging makes sense when the potential loss is significantly larger than the cost of the hedge.

Short-Term Volatility vs. Long-Term Trends

If you have a one-time payment due in 90 days, short-term volatility matters. Lock it in.

If you have recurring monthly payments over five years, short-term swings average out. Long-term trends matter more than daily fluctuations. In this case, natural hedging (matching revenues and expenses in the same currency) is often more effective than rolling over financial hedges every month.

Industries Where Hedging is Essential

Import/export-heavy businesses: If your gross margin is thin and a large portion of your revenue or cost base is foreign-denominated, hedging is not optional. One bad quarter of currency movements can eliminate profitability.

Project-based businesses with fixed-price contracts: If you commit to deliver a project at a fixed price and your costs are partially foreign-denominated, you are locked into the revenue but exposed on the cost side. Hedge the exposure at the time you sign the contract.

Businesses with long payment cycles: If you invoice clients today but collect payment in 90 to 180 days, the FX rate at invoice time may be very different from the rate at payment time. Hedge if the exposure is material.

Industries Where Hedging is Optional

Mostly local operations: If you buy and sell locally, FX movements do not affect your core business. You may have occasional foreign payments (software subscriptions, overseas travel), but these are immaterial. Accept the risk.

High-margin businesses: If your margins are 30 to 40 percent, a 5 percent currency swing is uncomfortable but not catastrophic. You may choose to self-insure rather than pay hedging costs.

Managing FX Risk in Bizrah

If you operate in multiple currencies, tracking your exposure is the first step. Bizrah gives you real-time visibility into multi-currency transactions without manual reconciliation or complex spreadsheets.

Track multi-currency transactions in real-time: Bizrah automatically records transactions in their original currency and converts them to your reporting currency at the prevailing exchange rate. You see both the original amount and the home currency equivalent on every transaction.

Automatic exchange rate updates: Bizrah pulls live exchange rates daily so your reports always reflect current market conditions. No need to manually update rate tables or hunt for yesterday's spot rate.

Realized vs. unrealized gains and losses reporting: Bizrah separates realized FX gains and losses (from settled transactions) from unrealized gains and losses (from open receivables and payables). You know which FX impacts have hit your cash flow and which are still on paper.

Multi-currency P&L visibility: Generate profit and loss statements in any currency. See how each currency contributes to overall profitability. Identify which currencies are creating exposure and which are naturally hedged.

No manual exchange rate tables: Most accounting systems require you to manually enter exchange rates for every transaction or maintain rate tables by date. Bizrah automates this entirely. Rates are fetched, applied, and stored without manual input.

See how Bizrah handles multi-currency accounting in Arabic and English. Try Bizrah free for 14 days.

Related reading:

- Cash Flow vs. Profit: The Survival Guide — FX fluctuations affect cash flow timing

- Unpacking the Income Statement — Where FX gains and losses appear in financial statements