Depreciation Accounting Explained: Methods, Examples, and Best Practices

Depreciation Accounting Explained: Methods, Examples, and Best Practices

Your 100,000 SAR delivery van does not cost 100,000 SAR this year.

You bought an asset. You paid cash. But that is not how the expense shows up in your books.

This is where many business owners get confused. You write the check, you own the asset, but your accountant tells you the cost gets spread across five years. That feels wrong.

It is not.

Depreciation is not an accounting trick. It is an attempt to match the cost of an asset with the years it generates revenue. The van you bought today will help your business for the next five years. So the cost should reflect that reality. Not the single moment you signed the purchase order.

What Depreciation Really Means (and Why It Matters)

Depreciation is the systematic allocation of an asset's cost over its useful life.

That is the textbook definition. Here is what it means in practice:

When you buy a laptop for 5,000 SAR that you will use for three years, you do not expense 5,000 SAR today. You expense roughly 1,667 SAR per year for three years. Each year, your income statement shows the portion of the laptop's cost that matched that year's use.

This creates a gap between cash flow and accounting. You paid 5,000 SAR upfront. But your profit and loss statement only recognizes 1,667 SAR of expense in year one. That gap confuses founders who manage by bank balance instead of by financial statements.

The reason this matters goes beyond accounting accuracy. In the GCC, businesses following IFRS for SMEs or local corporate tax rules must depreciate assets properly. Get it wrong and your taxable income calculation breaks. That turns into overpaid tax or audit risk depending on which direction the error goes.

If you are new to accounting fundamentals, read our guide on accounting for non-accountants first.

The Four Main Depreciation Methods

There are four main methods. You will likely use two of them.

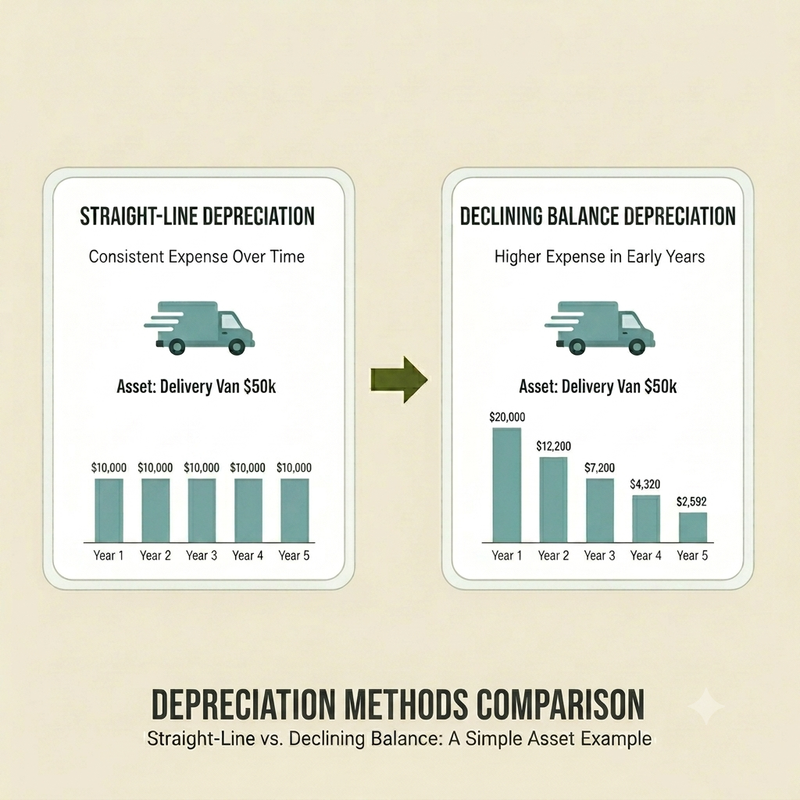

Straight-Line Method

This is the simplest and most common method for GCC SMEs.

Formula: (Cost - Salvage Value) / Useful Life

Example: You buy office furniture for 50,000 SAR. You expect to use it for 10 years. You estimate you can sell it for 5,000 SAR at the end.

Annual depreciation = (50,000 - 5,000) / 10 = 4,500 SAR per year

Every year for 10 years, you recognize 4,500 SAR of depreciation expense. The asset's book value decreases by 4,500 SAR annually until it reaches 5,000 SAR.

When to use: Buildings, furniture, standard office equipment. Anything that provides consistent utility over time.

Declining Balance Method

This method front-loads depreciation. You recognize more expense in the early years and less later.

Formula: Book Value × Depreciation Rate

The depreciation rate is typically double the straight-line rate (hence "double declining balance").

Example: Same 50,000 SAR furniture, 10-year life. Straight-line rate is 10% per year. Declining balance rate is 20%.

Year 1: 50,000 × 20% = 10,000 SAR

Year 2: (50,000 - 10,000) × 20% = 8,000 SAR

Year 3: (40,000 - 8,000) × 20% = 6,400 SAR

Each year the base shrinks, so the depreciation amount decreases.

When to use: Assets that lose value faster in early years. Technology, vehicles, specialized equipment.

Units of Production

This method ties depreciation to actual usage, not time.

Formula: (Cost - Salvage Value) / Total Estimated Units × Units Produced This Period

Example: A delivery truck costs 100,000 SAR. You expect it to last 500,000 kilometers. This year you drove 80,000 kilometers.

Depreciation = (100,000 - 10,000) / 500,000 × 80,000 = 14,400 SAR

If you drive less next year, depreciation drops. If you drive more, it increases.

When to use: Manufacturing equipment with measurable output. Vehicles tracked by mileage. Machinery with production cycles.

Sum-of-Years'-Digits

This is an accelerated method similar to declining balance but uses a different calculation. You will rarely see this in GCC SME accounting. Most businesses stick to straight-line or declining balance.

How to Choose the Right Method

The method you choose affects both your reported profit and your tax liability.

Start with the asset type:

- Buildings: straight-line (they do not lose value faster early on)

- Vehicles: declining balance or units of production (they depreciate faster when new)

- Office equipment: straight-line (consistent utility)

- Heavy machinery: units of production if you track usage, declining balance otherwise

Consider regulatory requirements:

In the UAE, Ministerial Decision No. 116 of 2023 allows businesses to choose depreciation methods but requires consistency. You cannot switch methods year-to-year to manage taxable income.

In Saudi Arabia, ZATCA recognizes both straight-line and declining balance methods. The method must align with the asset's actual economic use.

Think about tax timing:

Declining balance gives you larger deductions early. That reduces taxable income sooner. If you expect higher profits in future years, you might prefer straight-line to smooth out the deduction.

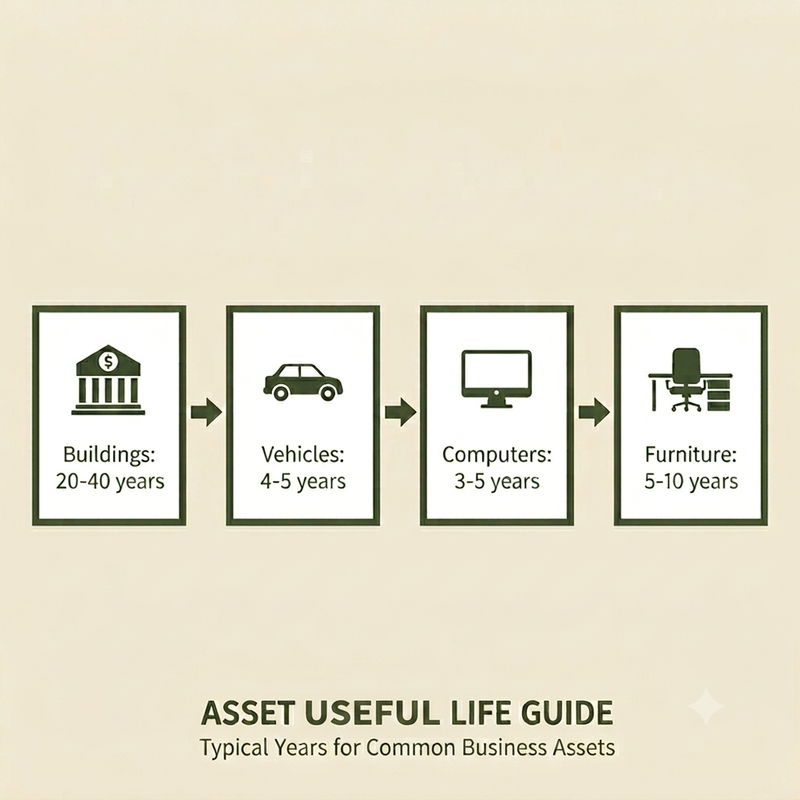

Depreciation in Practice: Common GCC Examples

Different asset types have different standard useful lives.

These are guidelines, not rules. A construction company's vehicle will depreciate faster than a logistics company's vehicle due to harsher conditions. Adjust useful life based on your actual use.

What Not to Depreciate

Not every long-term asset gets depreciated.

Land: Land does not wear out or lose utility. You carry it at cost on your balance sheet indefinitely. When you buy a property for 3,000,000 SAR and the land portion is 1,000,000 SAR, you only depreciate the 2,000,000 SAR building.

Inventory: Inventory is a current asset. You expense it through cost of goods sold when you sell it, not through depreciation.

Low-value assets: Most GCC businesses set a materiality threshold. If an asset costs less than 5,000 or 10,000 SAR, you expense it immediately rather than tracking depreciation for years. The administrative burden is not worth the accounting precision.

Assets under construction: You start depreciating an asset when you put it into service, not when you buy it. If you are building a warehouse over 18 months, depreciation starts when construction finishes and you begin using the warehouse.

Recording Depreciation: The Journal Entry

Depreciation is a non-cash expense. You are not paying anyone. You are recognizing that an asset's value decreased.

The journal entry:

Debit: Depreciation Expense 4,500 SAR

Credit: Accumulated Depreciation 4,500 SAR

Depreciation Expense is an income statement account. It reduces your profit this period.

Accumulated Depreciation is a contra-asset account on the balance sheet. It offsets the asset's original cost.

If you bought furniture for 50,000 SAR and have recognized 9,000 SAR of accumulated depreciation, the balance sheet shows:

Furniture (at cost): 50,000 SAR

Less: Accumulated Depreciation: (9,000 SAR)

Net Book Value: 41,000 SAR

The furniture's net book value is 41,000 SAR. That is its accounting value, not its market value. Those two numbers rarely match.

You record this entry every month or at the end of every quarter. Most businesses using cloud accounting software automate it. The system knows the asset's cost, useful life, and method. It calculates and posts depreciation automatically.

When Depreciation Goes Wrong

The most common mistakes:

Using the wrong useful life: You depreciate a laptop over 10 years because you saw "Office Equipment: 10 years" in a table. But laptops wear out faster than desks. Use realistic estimates.

Forgetting salvage value: If you plan to sell the asset at the end of its life, subtract salvage value from the cost before calculating depreciation. Depreciating the full cost overstates your expense.

Not adjusting for partial years: You buy an asset in July. You do not depreciate a full year in year one. You depreciate six months. This is basic, but businesses forget.

Continuing to depreciate fully depreciated assets: Once accumulated depreciation equals the asset's cost minus salvage value, you stop. The asset stays on your balance sheet at its salvage value until you dispose of it.

The Bottom Line

Depreciation is not optional. It is required under IFRS, local GAAP, and tax law across the GCC.

The method you choose affects your profit, your tax liability, and your balance sheet strength. Most SMEs default to straight-line because it is simple. That works for most assets.

If you operate in a capital-intensive industry or you hold assets that lose value quickly, declining balance or units of production may better reflect reality.

The key is consistency. Pick a method that matches the asset's economic use. Apply it every year. Document your rationale. And automate the calculation so you do not spend time each month doing depreciation math by hand.

Bizrah tracks fixed assets and calculates depreciation automatically using the method you choose. See how it works