Managing Multi-Currency Gains and Losses: A Practical Guide for GCC Businesses

Managing Multi-Currency Gains and Losses: A Practical Guide for GCC Businesses

When exchange rates move, your books need to move with them. Here is how to handle it without losing control.

Why This Matters for GCC Businesses

If you run a business in the Gulf, you probably deal with multiple currencies every week.

You invoice clients in USD because that is what they prefer. You pay suppliers in EUR because they ship from Europe. You hold SAR or AED for local operations. And every time an exchange rate shifts, the value of those balances changes.

That is not just a theoretical problem. It shows up in your financials.

Ignore it, and you end up with inaccurate profit figures, surprise losses at year-end, and a CFO who cannot explain why the books do not match reality. Handle it properly, and you get clean financials, predictable closes, and no surprises when auditors ask questions.

This is not advanced accounting. It is basic hygiene for any business that holds foreign currency.

When Currency Movements Hit Your Books

There are two types of foreign exchange (FX) impacts you need to track: realized and unrealized gains and losses.

The difference matters because they show up in different places, at different times, and with different tax implications.

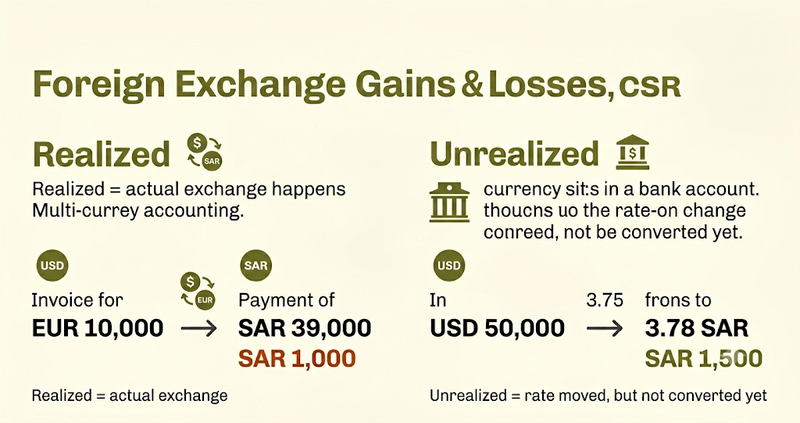

Realized Gains and Losses

A realized gain or loss happens when you actually exchange currency and lock in the rate.

Example: You invoice a European client for €10,000 when the rate is 1 EUR = 4.00 SAR. That is SAR 40,000 on your books. Sixty days later, they pay, but the rate moved to 1 EUR = 3.90 SAR. You receive SAR 39,000.

You just realized a loss of SAR 1,000.

That loss is real. It hit your bank account. It goes on your income statement immediately and affects your profit for the period.

Unrealized Gains and Losses

An unrealized gain or loss happens when you still hold foreign currency, but the exchange rate moved since you recorded the balance.

Example: You have USD 50,000 sitting in your bank account. When you first received it, the rate was 1 USD = 3.75 SAR (SAR 187,500 on your books). At month-end, the rate is 1 USD = 3.78 SAR. That same USD 50,000 is now worth SAR 189,000.

You have an unrealized gain of SAR 1,500.

It is unrealized because you have not converted the USD yet. If the rate moves again tomorrow, the gain could disappear. But your books need to reflect the current value, not the historical one.

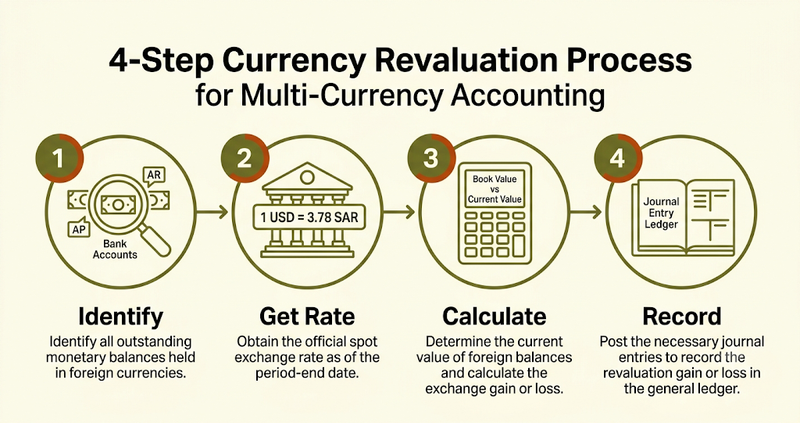

The Revaluation Process

Revaluation is the process of updating the value of your foreign currency balances to reflect current exchange rates.

You do this at every close: month-end, quarter-end, year-end. If you skip it, your balance sheet drifts away from reality, and your financials lose credibility.

What Gets Revalued

Foreign currency bank accounts

Accounts receivable (AR) denominated in foreign currency

Accounts payable (AP) denominated in foreign currency

Petty cash or advances in foreign currency

The Mechanics

Here is the process:

Identify all foreign currency balances — AR, AP, bank accounts, anything not in your functional currency

Get the current exchange rate — Use the rate from your central bank (SAMA for Saudi, UAE Central Bank for UAE), or the rate your bank uses for settlement. Do not use random rates from Google. Pick a source and stick with it.

Calculate the difference — Compare the book value (what you recorded at the historical rate) to the current value (what it is worth today)

Record the gain or loss — Journal entry to adjust the balance

Example:

You have USD 100,000 in AR. You recorded it at 3.75 SAR/USD (SAR 375,000). Today the rate is 3.78 SAR/USD. Current value: SAR 378,000.

Unrealized gain: SAR 3,000.

How to Record It

Realized Gains and Losses

When you actually convert currency or settle a transaction, you record the realized gain or loss.

Journal entry for a realized loss:

The loss goes to your income statement under "Other Expenses" or "Financial Expenses," depending on your chart of accounts.

Unrealized Gains and Losses

At month-end, you revalue your foreign currency balances and record the unrealized gain or loss.

Journal entry for an unrealized gain:

This also goes to your income statement, usually under "Other Income" or "Financial Income."

Tax note: In most GCC jurisdictions, realized gains and losses affect your taxable income. Unrealized gains and losses may or may not, depending on the country and your accounting method. Check with your accountant or tax advisor.

Practical Strategies to Minimize Exposure

You cannot eliminate FX risk entirely, but you can reduce it.

1. Invoice in Your Functional Currency When Possible

If you are a Saudi business, try to invoice in SAR. If you are in the UAE, invoice in AED. You push the FX risk to the customer.

This does not always work (especially with international clients), but when it does, it saves you from chasing rates.

2. Match Currency for Revenue and Expenses

If you earn revenue in USD, try to pay expenses in USD. This is called a natural hedge. When the rate moves, both sides move together, and the net impact on your profit is smaller.

Example: You invoice a US client in USD and pay a US supplier in USD. The rate between USD and SAR can swing, but your margin stays stable.

3. Set Clear Payment Terms

The longer the gap between invoice and payment, the more time the rate has to move against you.

Shorten your payment terms. Offer early payment discounts. Get paid faster, and you lock in rates before they shift.

4. Use Accounting Software That Handles Multi-Currency

Manual revaluation is tedious and error-prone. Modern accounting software tracks multiple currencies, applies the correct rates, and automates revaluation at month-end.

If you are still doing this in Excel, you are wasting time and risking mistakes.

Common Mistakes

Not Revaluing at Month-End

You cannot skip revaluation and hope it evens out. It does not. Your balance sheet becomes inaccurate, and your profit gets distorted.

Using Outdated Exchange Rates

Do not use last month's rate. Do not guess. Use the rate from your central bank or your bank's settlement rate, and use it consistently.

Forgetting About Petty Cash in Foreign Currency

If you have USD 500 in a drawer for travel expenses, that counts. Revalue it.

Not Documenting Which Rate You Used

Your auditor will ask. Your accountant will ask. Document the source and date of every rate you use.

Mixing Up Realized and Unrealized

Realized goes on the income statement when you settle the transaction. Unrealized goes on the income statement when you close the period. Do not confuse them.

What Your Accountant Should Handle

Some parts of FX accounting are beyond the scope of what most business owners should manage:

Tax treatment of unrealized gains and losses — varies by jurisdiction

Hedging strategies — forward contracts, options, swaps

Complex derivative accounting — if you are using financial instruments to hedge, your accountant needs to handle that

Stick to the basics: track your balances, revalue at month-end, and let your accountant handle the edge cases.

See how Bizrah handles multi-currency accounting automatically — revaluation, gains, losses, all tracked in real-time. Learn more →